[Live Prices USD]

Gold: |

Silver: |

Platinum: |

Palladium: |

Gold To Silver Ratio:

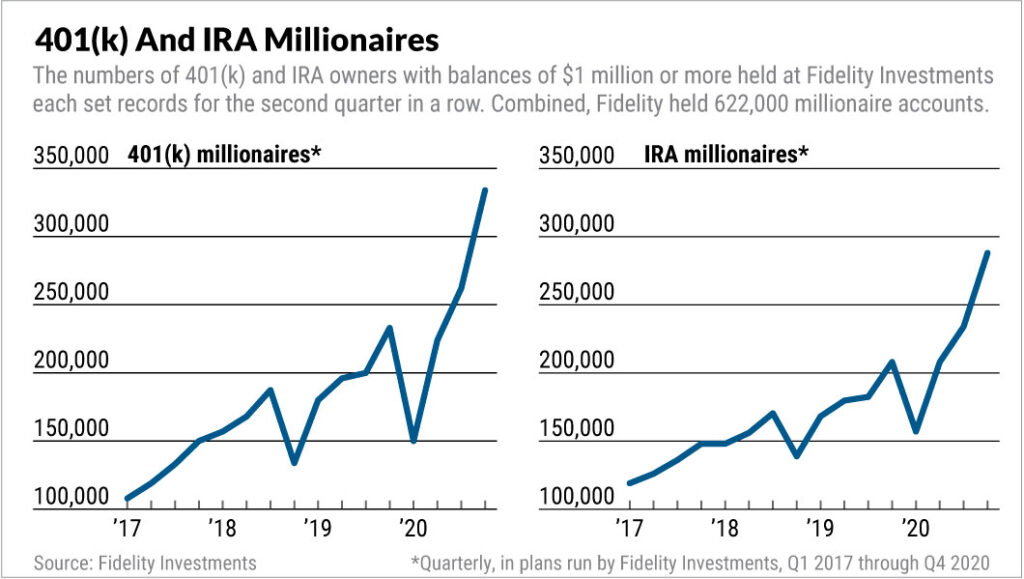

Retirement Balances Hit Records, So Do Ranks Of 401(k) And IRA Millionaires

PAUL KATZEFF 02/18/2021

Millions of Americans’ retirement savings hit record balances by the end of the fourth quarter of 2020. Likewise, the number of IRA millionaires and 401(k) millionaires also set record highs. Envious? A Fidelity Investments expert offers retirement planning tips for how you can boost your savings too.

First, feast your eyes on the results. The average balance in a 401(k) plan administered by Fidelity Investments reached $121,500. That was an 11% increase from the prior quarter. And it beat the prior record of $112,300 from 2019’s fourth quarter by 11%.

The 2020 fourth-quarter average IRA balance of $128,100 marked a 9% increase from 2020’s third quarter average balance of $117,700. That was the prior record.

Retirement Savings: Number Of Fidelity Investments Accounts With $1 Million Or More

And the number of retirement savings accounts with balances of $1 million or more also soared.

Millionaire 401(k) accounts cracked the 300,000 mark, reaching a record total of 334,000. That was a hefty 27% increase over the prior high-water mark, which was 262,000 millionaire 401(k) accounts as of the third quarter of 2020.

Similarly, the number of IRA millionaires reached a new peak of 288,000 as of Dec. 31. That topped the prior record of 234,000, which was set one quarter earlier.

Why 401(k), IRA Balances Rose

Retirement savers achieved those landmarks with help from a strong fourth-quarter stock market.

And retirement savers helped their own cause by doing three key things smartly. They:

- Saved persistently, sticking to long-term savings despite market and political volatility.

- Resisted the temptation to borrow and withdraw early from savings accounts despite new rules that made it less costly to do so.

- Invested aggressively, in age-appropriate securities.

Are You Maximizing Your 401(k) And IRA Contributions?

Kept Saving Despite Volatility

One sign of savings persistence was the fact that the average percentage of pay contributed to 401(k) accounts by workers in plans overseen by Fidelity rose to a record 9.1%. “Workers were not scared away by volatility,” said Eliza Badeau, vice president of the Fidelity Investments unit that studies behavior by plan members.

Another sign of persistence was that, despite 2020’s volatility, 33% of Fidelity 401(k) savers increased their retirement account contribution rate.

Resisting Temptation Helped Retirement Savings

It was also important that many savers resisted the temptation to tap their 401(k) accounts and IRAs, even though new federal rules waived the penalty for certain early withdrawals. “Ninety-four percent of savers on Fidelity platforms did not take those early withdrawals,” Badeau said.

Two Fidelity Investments Funds

As for aggressive investing, that translates to investing in age-appropriate ways. “For young investors, that means investing in stocks and stock funds,” Badeau said.

One way that more savers do that is by investing through target date funds. That helps many savers avoid what used to be a common error: parking contributions in cash and bond funds for decades, where the money grows far more slowly than in stock funds. “Compound growth over extended periods of time is one of the best tools that retirement savers can put to work for themselves,” Badeau said.

How much should workers invest in stocks and stock funds? “That depends on their time horizon, risk tolerance and goals,” Badeau said.

The $37.6 billion Fidelity Freedom Fund 2030 (FFFEX), which caters to investors who plan to retire in nine years, has 42% of its shareholders’ money in U.S. stock funds, 28% in international stock funds and 30% in bond funds.

The $2.8 billion Freedom Fund 2060 (FDKVX), which suits much younger investors who won’t retire for another 39 years, has 54% of its assets in U.S. stock funds, 36% in international stock funds and just 10% in bond funds.

More Steps To Boost Retirement Savings

What else can you do to boost your retirement savings? In addition to persistence, discipline and age-appropriate investing, Badeau recommends two steps:

- Start early. “Time is your best friend as a saver,” Badeau said. The more time you have, the less money you must invest to reach any given goal. Similarly, the more time you have, the lower your annual rate of return can be while pursuing your target end balance.

- Save enough. That means aiming to save 15% of your pay each year. “That can include any company match you receive,” Badeau said. “So always save enough to earn your employer’s maximum match. It’s never a good idea to leave money on the table.”

- And don’t worry if you can’t start with a savings rate of 15%. “You can always make small incremental increases in your savings rate,” Badeau said. “Even increases of one percentage point a year add up over time.”

Long-Term Fidelity Investments Savers

One additional indication of the benefit of persistence, discipline and age-appropriate investing in retirement accounts is how fast average balances have soared.

Ten years ago — as of Dec. 31, 2010 — the average Fidelity Investments 401(k) account balance was just $69,700. Today’s average balance is 74% higher.

Today’s average IRA balance is 84% higher than it was a decade ago.

Similarly, when Fidelity number crunchers isolate long-term savers from savers overall, the benefit of stick-to-itiveness is clear.

The average 401(k) account balance for savers who have been in their plan for 10 years in a row rose to $370,400. That was up from $310,300 a year ago.

Protect & Secure Your Retirement Savings Now!

Includes: Printed Guide, Audio Guide & Video Guide

Request Your Free Kit!

A title

Image Box text

Protect & Secure Your Retirement Savings Now!

Includes: Printed Guide, Audio Guide & Video Guide

Request Your Free Kit

Key benefits of a Self-Directed IRA are that rollovers from most other types of retirement accounts. For example, investors with pension plans, annuities, 401(k)s, 403(b)s, 457(b)s, or Thrift Savings Plans (TSP) are ALL allowed.